22 April, 2020

Hui Min Ng, Portfolio Manager

The global spread of COVID-19, coupled with a notable deceleration in economic activity, are posing challenges for Asia-Pacific Real Estate Investment Trusts (AP REITs). In this investment note, Hui Min Ng, Portfolio Manager, explains why active bottom-up fundamental research is more important than ever, especially when constantly changing government policies are leading to short-term price dislocations. Furthermore, the defensive properties of the asset class could make it more resilient in an economic downturn.

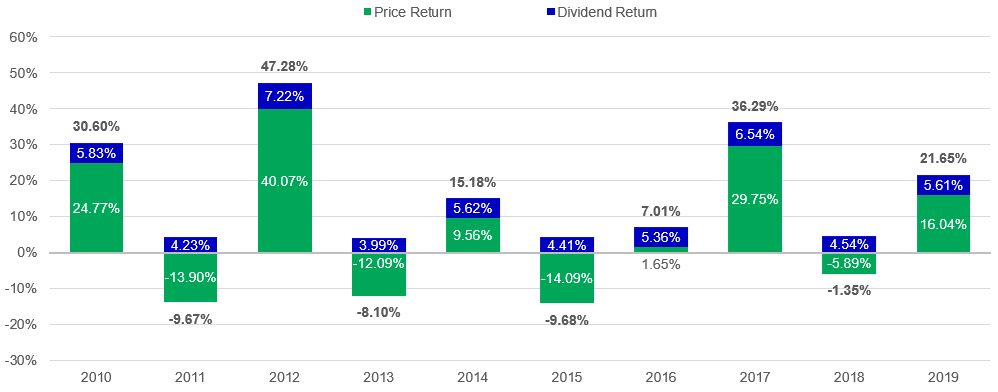

Before discussing the current challenging market environment, it is important to remember why people invest in REITs in the first place. REITs are a hybrid security. That is, even though REITs are traded like equities, with the possibility of price depreciation (loss), they also offer investors a regular income payout. As illustrated in chart 1, the income feature of REITs gives them their defensive properties, providing a buffer when markets move lower and enhancing your total return when markets appreciate.

From an economic perspective, the initial outbreak of COVID-19 led to a notable slowdown in Asian economic activity, centred on China. As time has progressed, the global spread of the virus has raised the spectre of a more prolonged economic downturn, including the possibility of a recession.

In addition to the assorted directives that aim to offset the burden on businesses, governments in the region have introduced various fiscal and monetary policy measures. These policies are constantly being updated given the efforts being made to contain the spread of the virus. This backdrop has created short-term uncertainty and resulted in share-price pressure for REIT managers.

The Fed starts easing: Potential tailwinds for high-quality US credits

Our analysis shows that US IG credits and preferred securities have historically performed well following US Federal Reserve (Fed) rate cuts. We maintain our favourable view of asset classes that offer unique investment opportunities for fixed-income investors looking for potentially attractive returns.

The Fed’s rate decision: Not so surprising, but what’s the path forward?

We see three important themes worth highlighting now that the Fed’s easing cycle is finally underway.

After elections: What’s next for India?

We analyse the implications of the recent pivotal election and lay out a roadmap for how it may affect India’s economic development and investment opportunities through the ‘5Ds’ framework.

During these times, we believe that fundamentals matter more than ever. Our focus remains on capital strength, the pedigree of the sponsor, and drilling down to the details of lease terms and structure.

We also think that AP REITs are better positioned to face the current economic downturn than they were after the global financial crisis (GFC). Stronger balance sheets mean that the risk of REITs breaching debt covenants is lower, which suggests that the need for dilutive equity fund raising will be minimised.

We believe that AP REITs are more robust in three main areas:

Although this economic environment will inevitably pose challenges to AP REITs, particularly in the hotel and retail sectors, as well as REITs with a high exposure to small-and-medium enterprises (SME), we believe the asset class is still better positioned than it was during the GFC.

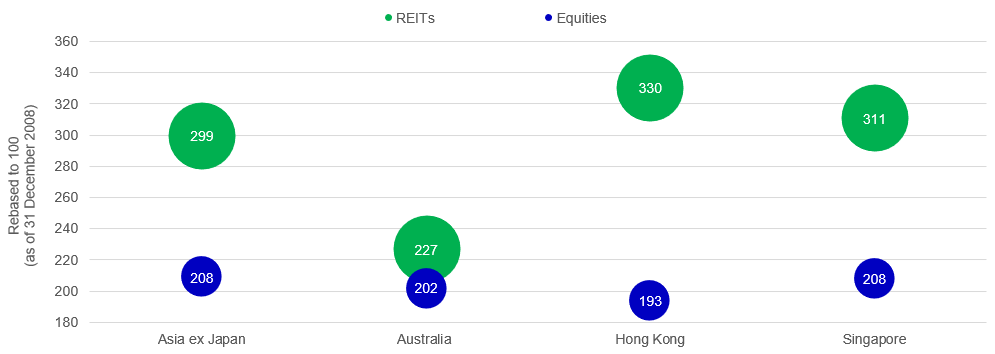

Historically, AP REITs have outperformed equities during periods of low interest rates (see Chart 2), which we have re-entered after the simultaneous demand-and-supply shocks imposed by the global spread of COVID-19.

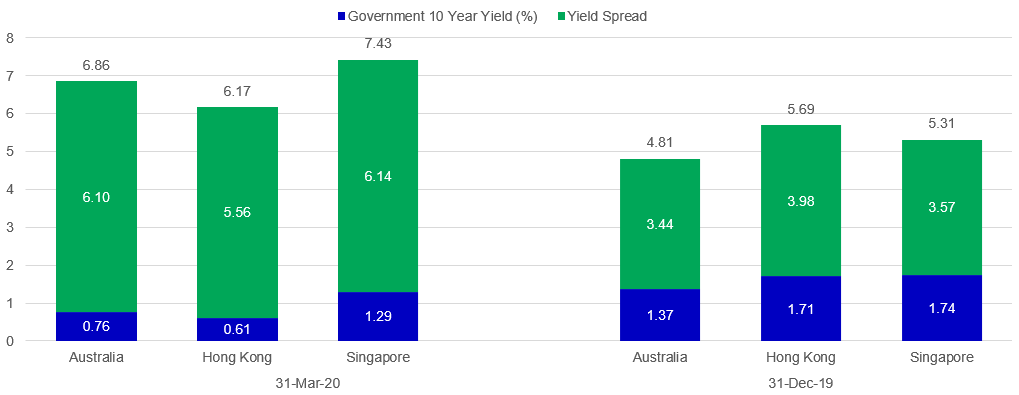

One of the main factors underpinning this outperformance is expanding yield spreads. A yield spread is the difference between the yield on, for example, a risk-free instrument (such as US Treasuries) and the yield offered by other issues. As risk-free rates move lower – they have been aggressively cut over the past month – investors are being compensated more for assuming risk.

Total Return (from 31 December 2008 – 31 December 2015)

Chart 3 shows yield spreads in the key AP REIT markets – Australia, Hong Kong, and Singapore – from the beginning of 2020 through early March: yield spreads have widened in all three, as the risk-free rate has fallen.

We believe that lower interest rates and the global search for yield among investors will continue to support the asset class.

Although REITs do have qualities that are defensive in nature, we believe that no segment in the REIT space should be considered “recession-proof”.

Given the current economic environment and recent government directives, there will be temporary disruption, particularly in the consumption and tourism-related industries. This has resulted in downward revisions to DPU estimates for 2020. However, we do believe that these revisions have been fully priced into share prices, as yield spreads are trading well above their 10-year averages4.

Investors may find opportunities in the following segments:

AP REITs are not immune from the economic fallout from the spread of COVID-19. However, the defensive characteristics of the asset class suggest that investors should benefit from their hybrid nature. At the same time, the fundamentals of AP REITs, including relatively robust performance in low interest-rate environments and an improved financial position, augurs a greater resiliency compared to other investments.

1 Source: Bloomberg, 31 March 2020.

2 Bloomberg, as of 30 November 2019. Gross total returns in US dollar. Past performance is not indicative of future performance. Australia REIT – S&P/ASX 200 A-REIT Index, Hong Kong REIT – Hang Seng REIT Index, Singapore REIT – FTSE ST Real Estate Investment Trusts index, Asia ex Japan REITs = FTSE EPRA/NAREIT Asia ex Japan REITs Index, Singapore Equities = Straits Times Index STI Total Return Index, Hong Kong Equities= Hang Seng Index, Australia Equities = S&P/ASX 200 index, Asia ex Japan equities= MSCI AC Asia Ex Japan index (total return).

3 Source: Bloomberg, 31 March 2020.

4 Source: Bloomberg, 31 March 2020. Singapore REITs = FSTREI Index, 10 year Singapore government bond. Australia REITs = AS51PROP Index, 10-year Australian government bond. Hong Kong REITs = HSREIT Index, 10-year HK government bond (data as of May 2012).

5 CapitaLand Investor Day 2019, 29 November 2019.

© 2025 Manulife Investment Management. All rights reserved.