20 July 2022

Kai Kong Chay, Senior Portfolio Manager, Greater China Equities

With the first half of 2022’s market events behind us, we see a brighter outlook for Chinese equities in the mid-year ahead. The government recently announced shortening quarantine times for inbound travellers and easing of lockdown measures — encouraging signs that more relaxation of restrictions is yet to come. Chinese equity markets are rebounding from valuation troughs amid improving market sentiment, lockdowns being lifted and a slew of stimulus measures.

With China’s pro-growth policies expected to continue, Kai-Kong Chay, Senior Portfolio Manager for Greater China equities, sees opportunities arise in three investment themes for the mid-year ahead: policy tailwinds, innovation, and consumption upgrade. Chay remains constructive, expecting policy executions to accelerate in the second half of the year, and believes that longer-term investors will be rewarded for participating in these sectorial opportunities.

As lockdowns began to ease towards the end of the second quarter, Chinese equity valuations are rebounding from multi-year lows. During the first quarter of 2022 – the peak of new COVID cases, global financial markets as well as China’s stock markets declined. Back then, it was a perfect storm of risk-off events: Russia-Ukraine geopolitical tensions, regulatory curbs on tech stocks, potential de-listing of the American depositary receipts (ADRs) of Chinese firms, and a looming hawkish U.S. Federal Reserve.

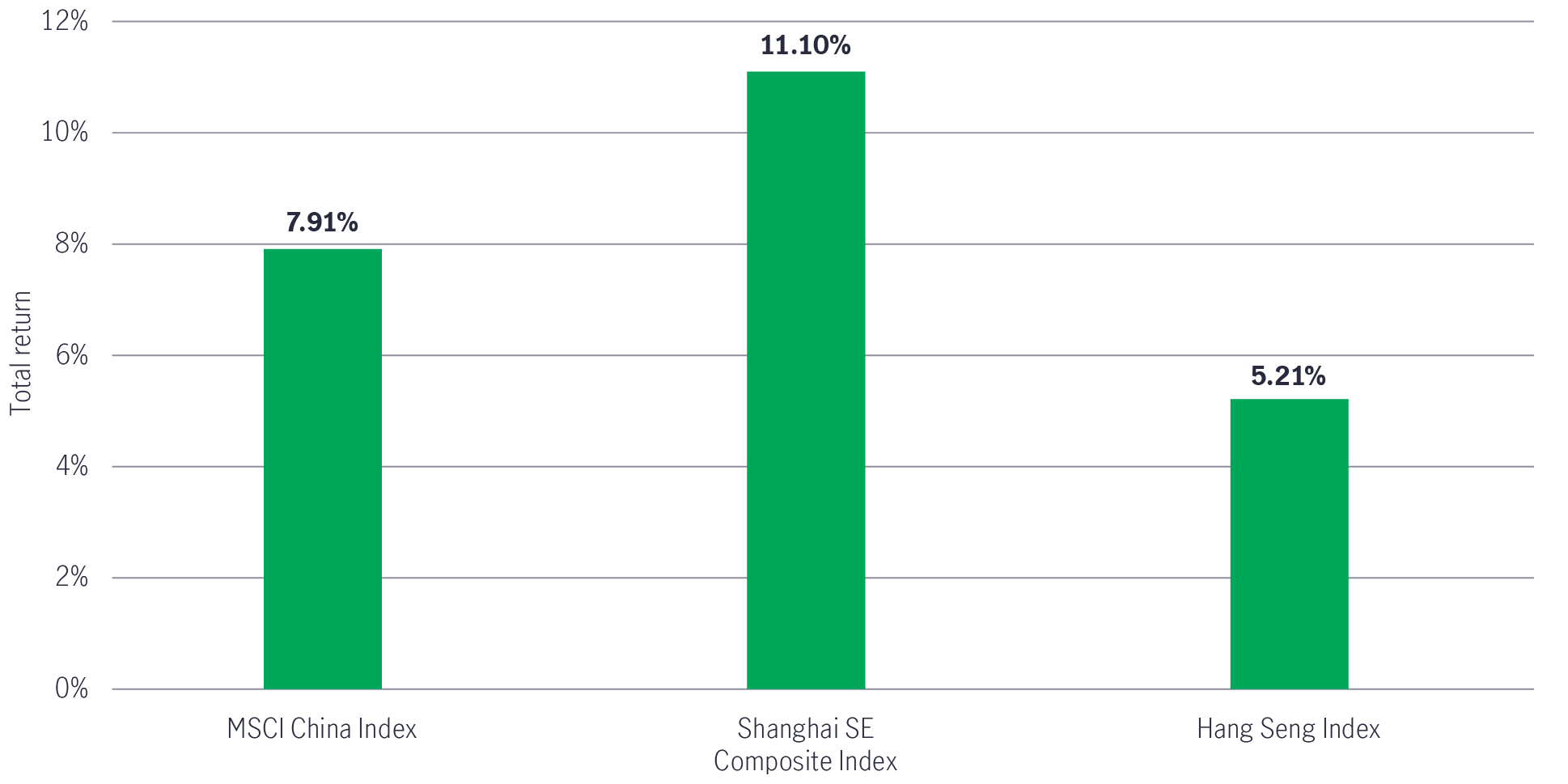

In the last two months, China’s stock markets have staged the first phase of a rebound (see Chart 1) on the back of a raft of relaxation measures: Investor sentiment has recovered as lockdown restrictions begin to ease; the Hong Kong government accelerated its reopening in May by cutting quarantine times for inbound travellers (from 14 days to 7 days) and eased social distancing measures. In June, China shortened quarantine times for those entering major cities, who will only need to spend 7 days in a quarantine facility, and 3 days of home quarantine (that’s down from 14 days of hotel-quarantine in many parts of China currently, and as many as 21 days of isolation in the past), according to a revised government protocol.1

Chart 1: China and Hong Kong stock markets rebounding from policy support (May 2022 – present)

Source: Bloomberg data from 29 April – 1 July 2022. Index performance based on total return in USD. It is not possible to invest directly in an index.

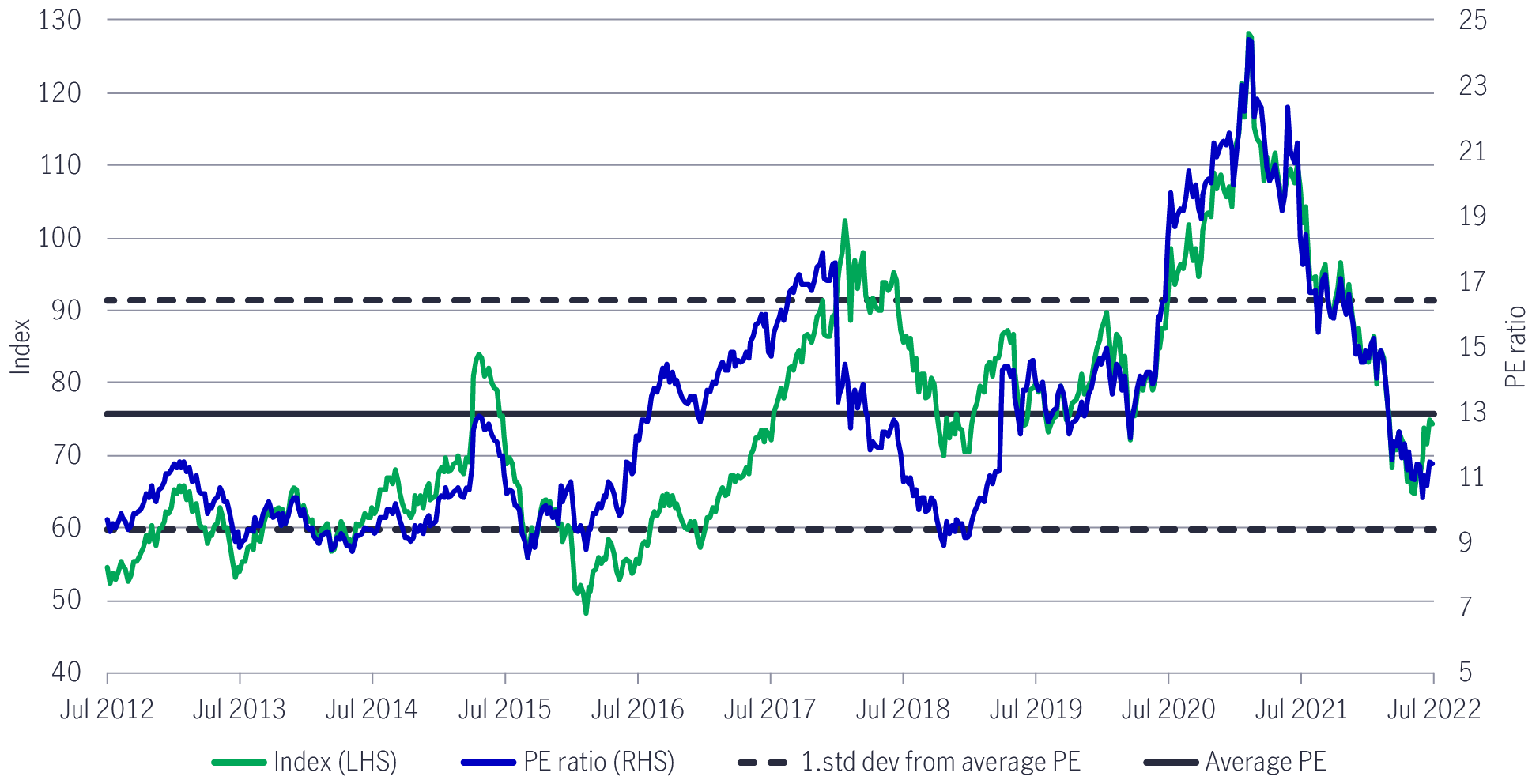

Chart 2: MSCI China Index performance and valuation (10-year)

Source: Bloomberg as of 1 July 2022. It is not possible to invest directly in an index.

At the time of writing, the MSCI China, Hong Kong and Chinese onshore A-shares indexes have rebounded since May and their price-to-earnings (PE) valuations have recovered from multi-year lows. We believe Chinese equities could have more room to run due to their attractive valuations that are below the historical average and near the bottom of the standard deviation range (see Chart 2). Also, we’re more constructive of the second half outlook which we’ll highlight in the next section.

China’s first-quarter GDP beat expectations and grew 4.8% year-on-year. We expect that for the remainder of this year, China should see a re-acceleration in GDP growth, while most of the Asia (ex-China) central banks are likely to raise rates on US dollar strength. Recent economic data such as China’s industrial output, exports, retail sales have been picking up and the purchasing managers’ index (PMI) for June rose above the expansionary territory of 50 — signs that factory productions are resuming, and pent-up domestic demand being released.2

A raft of economic stimulus measures was announced throughout the first half of 2022 (see Appendix), which shall permeate the real economy. Numerous sectors are expected to benefit from further macro-policy push in the second half, and with a stronger boost to consumption and easing supply-chain bottlenecks.

Investors might increasingly view China as a diversifier (of risks and returns). While global central banks are dealing with elevated inflation and rate hikes in the cards, China has been pursuing a divergent monetary policy: the central bank lowered the reserve requirement rate (RRR) by 25 basis points (bps),3 slashed the 5-year loan prime rate (LPR) by 15 bps and further reduced the mortgage rate floor for first-time homebuyers.

We believe China still has room to ease monetary policy further amid below-target inflation and support for the labour market. The property market has stabilised while further clarification is needed on two areas, i.e., when China would move on from dynamic zero COVID response and when the political landscape will settle following the 20th Party Congress.

In terms of fiscal policy, there is a decent probability that China’s National People’s Congress Standing Committee August meeting may approve additional fiscal stimulus, likely in the order of RMB$ 1 trillion. On 23 June, President Xi reiterated China’s commitment toward pre-established 2022 growth targets.

All in all, we believe that the fiscal and monetary stimulus announced in May 2022 set the stage for further economic recovery for the second half of the year, and markets have not fully priced in the more constructive outlook.

We identify three key investment themes for the mid-year that continue to benefit from continued policy support.

1. Policy tailwinds

Powering growth with renewable energy and auto stimulus

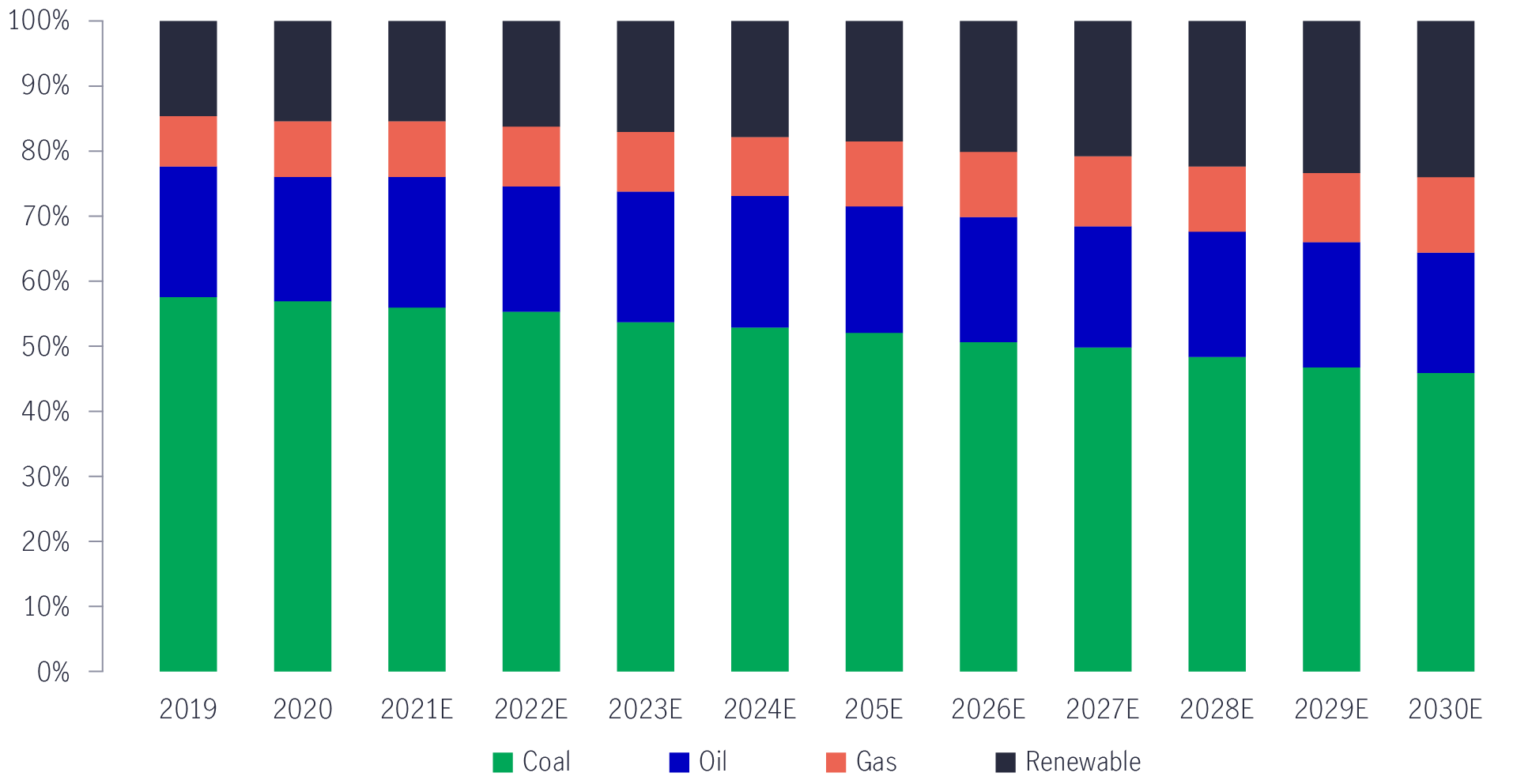

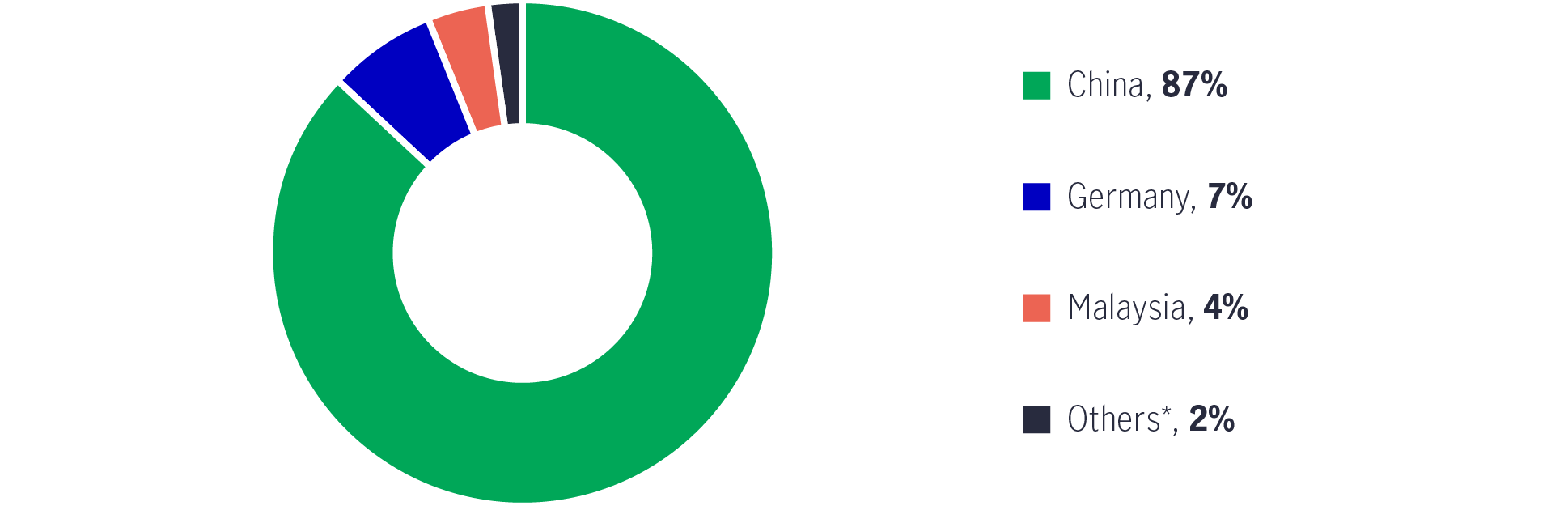

At a time when elevated oil prices push up global inflation, China has been making promising progress in tapping clean and alternative energy. On renewable energy, China aims for CO2 emissions to peak by 2030 and carbon neutrality by 2060. According to the National Development and Reform Commission, China plans to raise the share of non-fossil fuels in its primary energy mix to 25% by 2030, from 15.9% in 2020 and that total installed capacity of wind power and solar power could reach more than 1.2 billion kilowatts.4 (see Chart 3) We continue to see solid investment opportunities in the renewable energy sector. For example, China makes 87% of the world’s polysilicon (a vital component of the solar supply chain) installed capacity.5 (see Chart 4)

Chart 3: China’s primary energy consumption by source

Chart 4: Global polysilicon capacity breakdown

Source (Chart 3): BP statistics, Our World in Data, IEA, Daiwa as of September 2021. Renewable includes hydro, solar, wind, nuclear and biofuel. 2030 estimate based on National Development and Reform Commission target, as of January 2022. Source (Chart 4): BNEF, BofA Global Research, as of April 2022. For details of Others: see ReportLinker and Bernreuter Research reports.

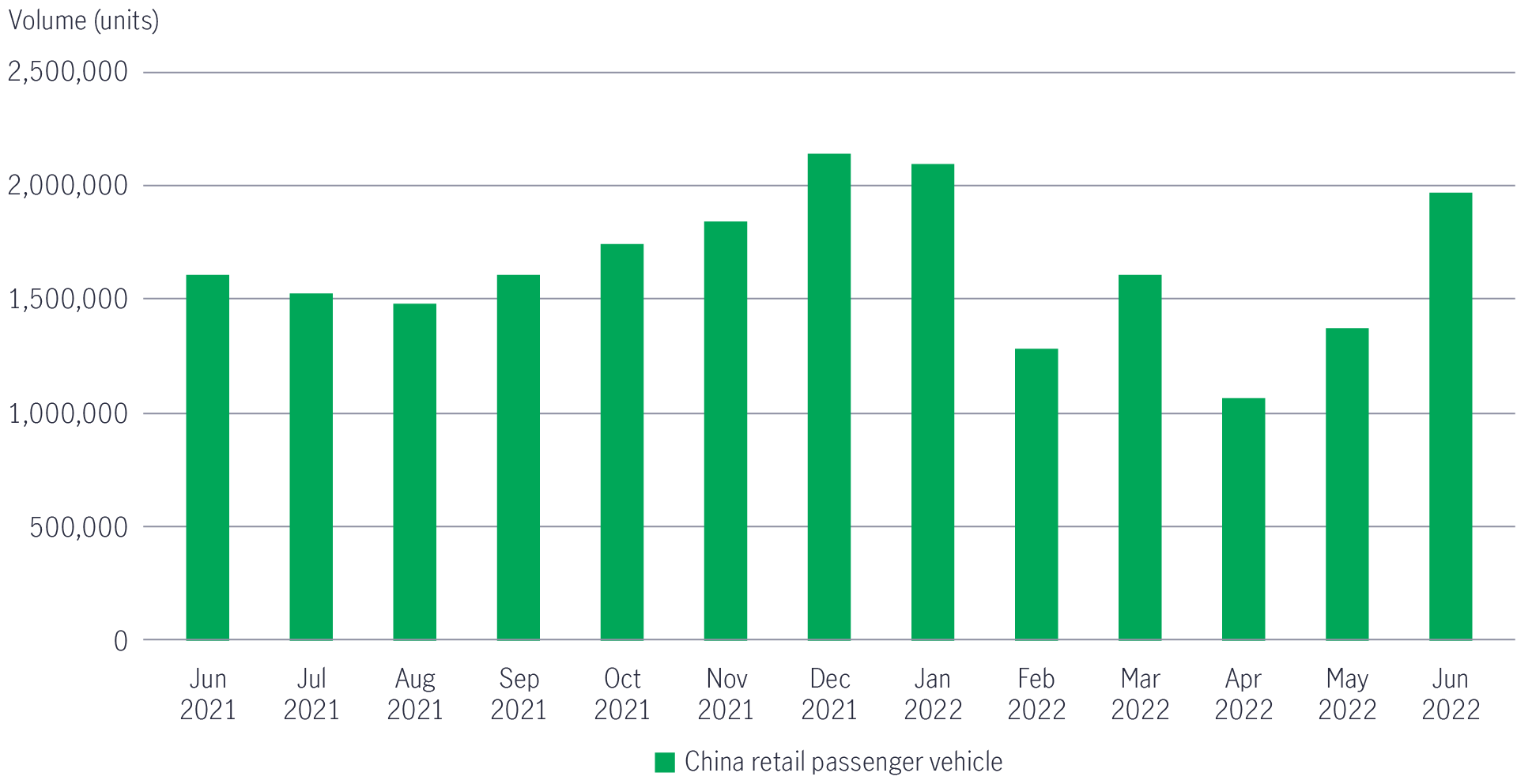

Another beneficiary of policy tailwind is the auto sector, a key contributor of China’s consumption growth. In May, authorities relaxed car-purchase restrictions and cut the purchase tax by half for small-engine passenger cars priced under RMB$300,000 with 2.0-litre or smaller engines. About 90% of engine vehicles in the market would likely be eligible for tax incentives.6 The tax cut was larger than expected and should benefit traditional auto manufacturers. Retail sales of passenger vehicles have already edged higher since the new tax policy, topping 1.96 million units (from 1 June to 30 June). (see Chart 5) We expect Chinese automakers will continue to accelerate their production and deliveries from June 2022 in anticipation of a demand recovery.

Chart 5: China retail passenger vehicle sales

Source: Bloomberg as of 13 July 2022.

On infrastructure spending, the State Council announced plans to use funds from the local government special bond (LGSB) programme to support a broader range of projects, including new infrastructure such as high tech and 5G.7 We believe infrastructure construction may accelerate in the third quarter of 2022 if the LGSB quota is used by June and could be fully utilised in projects by August 2022.

2. Innovation

As a digital economy and high-value global manufacturing hub

We continue to see opportunities that leverage the government’s agenda to develop a digital economy and China strengthening its position as a high-value global manufacturing hub, industrial automation and manufacturing upgrades led by advanced technology. Recently announced incentives support innovative growth:

With the growing adoption of renewable energy, such as solar and wind, we expect demand for battery storage of renewable energy or energy storage systems (ESS) to rise. Indeed, China’s installation of ESS is expected to grow at a 56% cumulative average growth rate over the next decade.9

In the longer term, we believe China will play a pivotal role in the global electric-vehicle (EV) supply chain, with EV battery manufacturers leading the way. The lithium ion-battery is the most important component of an electric vehicle, as it is the energy source; and Chinese companies make over half of the world’s EV batteries10 (see Chart 6) Outside of China, ASEAN markets are also developing their own EV supply chain, which provides opportunities for China’s companies that have exposure throughout the entire EV supply chain.

Chart 6: Importance of China’s battery supply chain in global market (2021 market share)

Source: Morgan Stanley, as of 3 January 2022. * For details of Other markets: see Bloomberg and Mining Intelligence reports.

There is also a growing list of other companies in the EV supply chain such as makers of components: battery precision parts, car charging stations, electric motors, automotive lens and sensors, and other EV-associated products. We think the long-term outlook for these EV component providers is also promising.

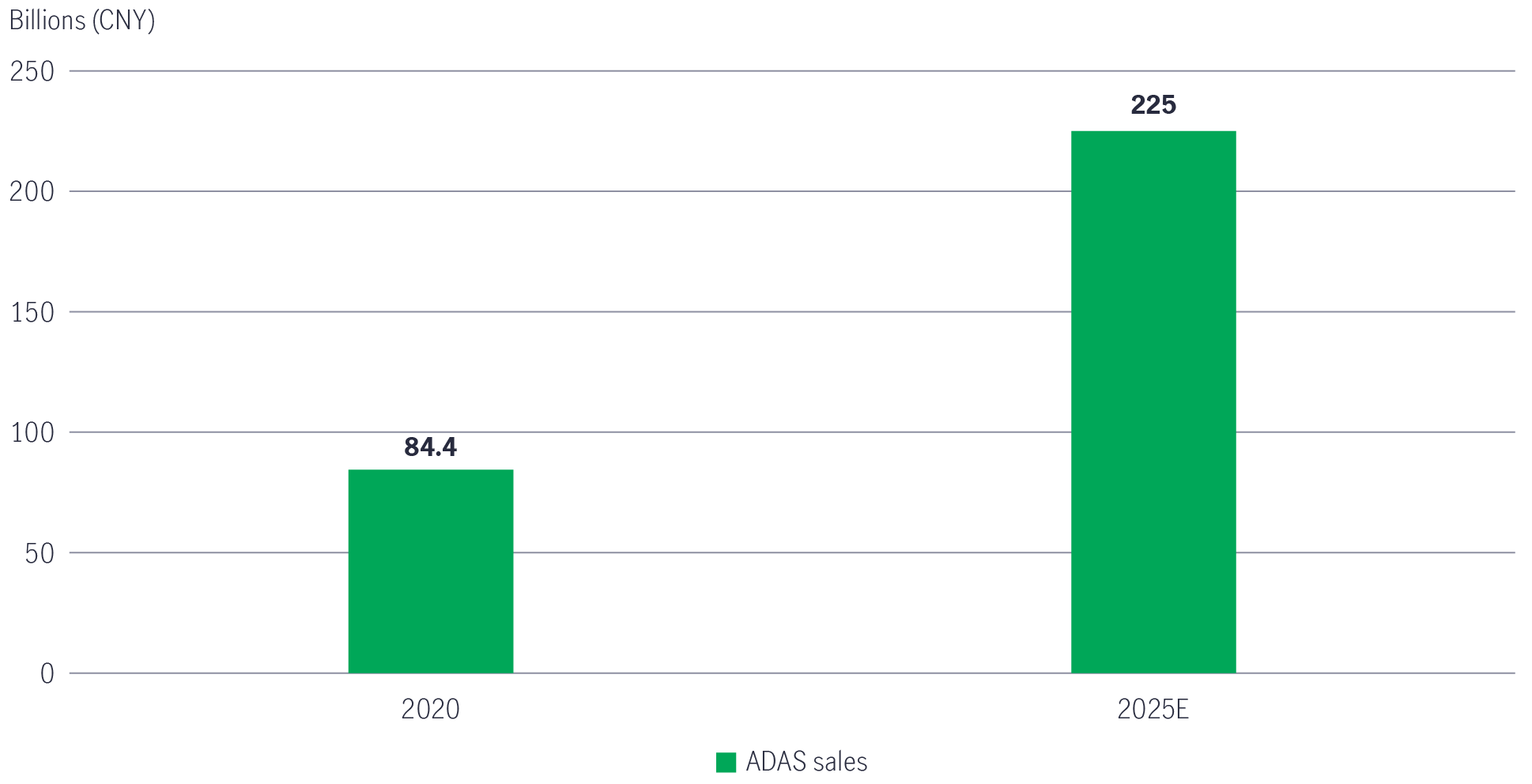

We believe Chinese makers of advanced driver assistance systems (ADAS), for example, are poised to benefit from a structural shift toward energy efficiency and changing consumption patterns of the younger generation. ADAS are applications and technologies that are installed into self-driving (autonomous) vehicles to serve multiple purposes from injury protection, pedestrian detection, night vision, road safety, cruise control to automatic parking. Components of an ADAS range from hardware or software, chips, sensors and radars to cameras and lens.

We predict ADAS suppliers will see growing penetration rate as the demand for autonomous vehicles increases and these assisted-driving technologies are installed. According to the projections of China Association of Automobile Manufacturers (CAAM), the country’s ADAS market recorded sales of CNY 84.4 billion in 2020 while industry reports expect the market to reach CNY 225 billion by 2025. (see Chart 7)

Chart 7: Advanced Driver Assistance System (ADAS) sales in CNY (billion)

Source: China Association of Automobile Manufacturers (CAAM), EqualOcean, as of 8 May 2022.

3. Consumption

Upgrading lifestyle and products amid changing demographics

With stimulus measures underway, we expect consumption growth to pick up in the year's second half. China’s travel, tourism, and hotel stocks are rebounding after the government announced the relaxation of travel rules and reopening of city lockdowns.11 Domestic consumption-related stocks including restaurant operators and local retail businesses are also benefiting as the government relaxes quarantine times for close contacts.

The free digital cash campaign launched in Shenzhen and Hebei may further stimulate the purchase of consumer electronics and home appliances. In Shenzhen, consumers will receive up to RMB$10,000 for each purchase of a new-energy vehicle, RMB$2000 for purchasing consumer electronics and RMB$2000 for home appliances.12

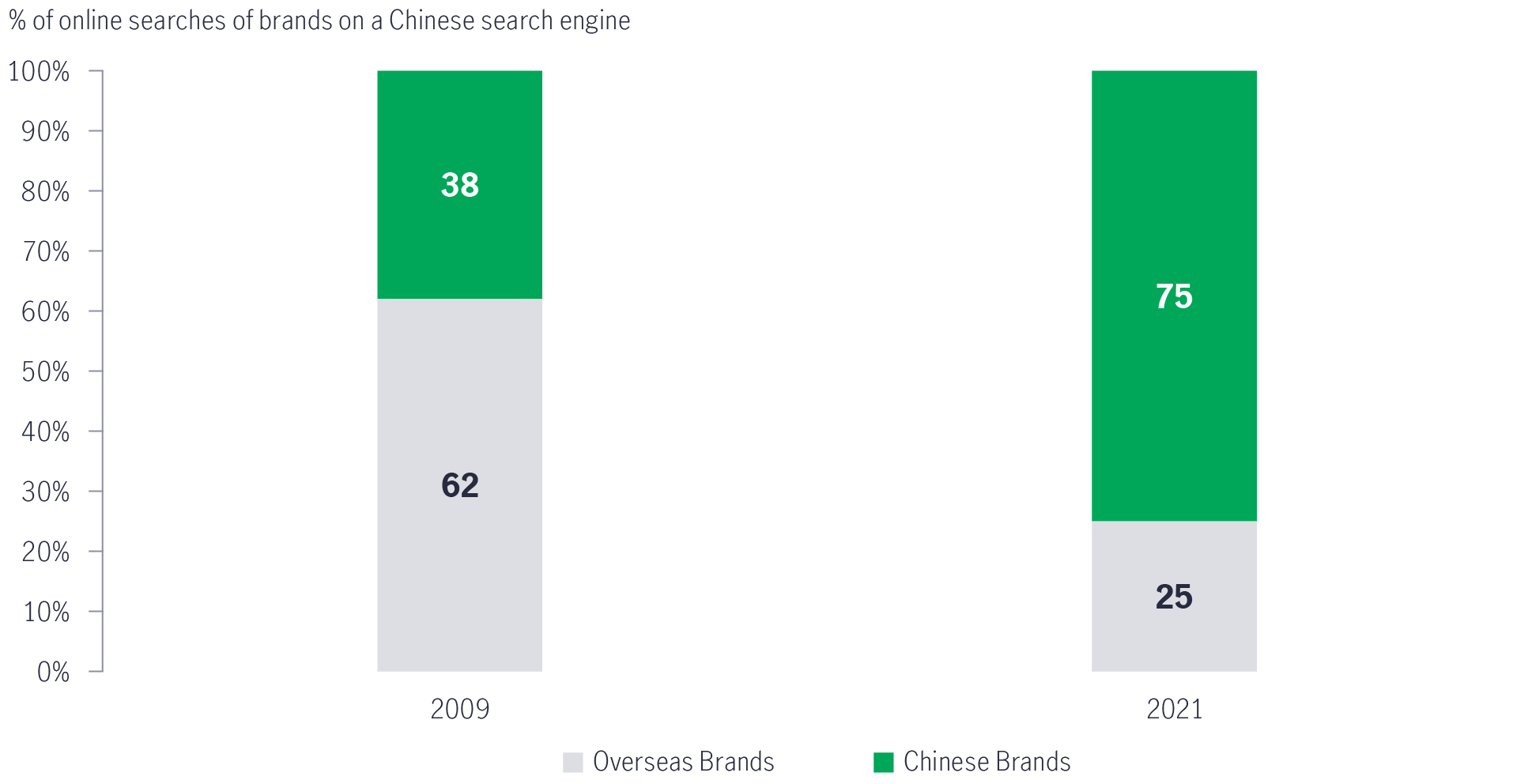

Furthermore, consumption growth will remain an ongoing theme in China, given a population of 1.4 billion and a growing middle-income class. Thanks to the rise of homegrown brands or “guochao”, Chinese domestic brands are fast gaining market share from foreign equivalents in several consumer categories, such as sportswear, skincare, and cosmetics. In cosmetics, for example, local brands are growing in popularity among the sophisticated younger consumers, who use social platforms to access skincare knowledge. (see Chart 8)

Chart 8: Domestic brands gaining attention

Source: Baidu, Research Institute of People.cn, as of May 2021.

We have already seen the V-shaped recovery that China’s economy experienced in 2021. The COVID-persistent environment makes it hard to find a quick resolve to economies affected by the pandemic, but we believe that China has been coping with these challenges progressively and is likely set for a gradual recovery. Thanks to the government’s fiscal and monetary policy support, we see structural sector themes and opportunities in Chinese equities. The country remains committed to carbon neutrality and is fast becoming a leader in the global EV ecosystem and in a dynamic and thriving consumption market. We believe that longer-term investors will be rewarded for their participation in these sectorial opportunities and benefit from asset-allocation and diversification perspectives. Meanwhile, a bottom-up, focused and stock picking approach is key to understanding China’s diverse equity universe.

| Fiscal measures13 | Objectives/sector beneficiaries |

| Expand the scope of businesses eligible for VAT credit rebates from 6 to 13 industries14 |

|

| Defer payments on some social- insurance programmes, subsidies for utility expenses and rentals, and financing support |

|

| Increase emergency loans to airlines by RMB$150 billion, funded with bond issuance of RMB$200 billion |

|

Streamline restrictions on the movement of trucks across regions Free access to COVID testing for cargo drivers Increase domestic and international passenger flights in an orderly manner, facilitate the travel of foreign companies’ employees |

|

| Relax car-purchase restrictions and reduce purchase taxes on select passenger cars |

|

Boost spending and guide banks to finance construction projects for irrigation facilities, transportation facilities, residential community renovation, rural road construction projects Support railway construction with bond issuance |

|

Assessing China’s Latest Stimulus Measures

Greater China Equities Team analyses the latest round of strategic stimulus and explains why it warrants more than short-term tactical attention. The team also highlights a case study of Chinese companies that are ‘going-global’ to showcase this interesting juncture in the country’s corporate development.

The Fed starts easing: Potential tailwinds for high-quality US credits

Our analysis shows that US IG credits and preferred securities have historically performed well following US Federal Reserve (Fed) rate cuts. We maintain our favourable view of asset classes that offer unique investment opportunities for fixed-income investors looking for potentially attractive returns.

The Fed’s rate decision: Not so surprising, but what’s the path forward?

We see three important themes worth highlighting now that the Fed’s easing cycle is finally underway.

| Monetary-policy measures | Objectives/sector beneficiaries |

| Reduced the RRR for most banks by 25 basis points and by 50 basis points for smaller lenders, effective 25 April |

|

| Provide funds to banks to encourage lending to small businesses |

|

| Defer principal and interest payments on small-business loans and truckers’ car loans, as well as mortgages and consumer loans for individuals experiencing temporary difficulties |

|

| Loosen minimum down-payment requirements, and cut mortgage rates |

|

| Lowered the 5-year loan prime rate (LPR) by 15 basis points to 4.45% and reduced the mortgage-rate floor for first-time homebuyers by 20 basis points on 15 May |

|

1 Source: China’s National Health Commission; Bloomberg, 28 June 2022

2 Global Times, “China’s export growth rebounds to 16.9% in May as epidemic outbreak wanes”, 9 June 2022. Statista, China: Manufacturing Purchasing Managers' Index 2022 as of 30 June 2022

3 Bloomberg, “China’s Central Bank Pledges Support for Businesses Amid Covid”, 18 April 2022

4 National Development and Reform Commission, “Nation moves ahead with ambitious climate goals”, 6 January 2022. IHS Markit, “China seeks to perform balancing act with latest national energy plans amid climate, supply risks”, 1 April 2022

5 BNEF, BofA Global Research, as of April 2022.

6 Fitch Ratings, “China Aims to Restore Car Demand with Strong Fiscal Stimulus”, 13 June 2022

7 The State Council Information Office of China (SCIO), “China speeds up future-oriented infrastructure development”, 12 May 2022

8 China Daily, “China relaxes restrictions, cuts taxes to boost auto sales”, 31 May 2022

9 Daiwa, as of January 2022.

10 Morgan Stanley report, "China Battery Supply Chain", as of 3 January 2022.

11 Bloomberg, 30 June 2022.

12 Global Times, “Shenzhen offers subsidies to NEV, home appliance and digital products buyers to boost consumption”, 26, May 2022.

13 Bloomberg, “These Are the 33 New Measures China Is Taking to Boost Growth", 23 May 2022.

14 China Briefing, “China Stimulus Policy - 33 New Support Measures for Boosting Growth”, 2 June 2022

© 2025 Manulife Investment Management. All rights reserved.