26 March 2024

Capital Markets Strategy Team, Manulife Investment Management

On paper, it is true that that for investors with a time horizon of greater than 10 years, it may not make sense to hold bonds as they underperform equities most of the time1. However, in reality, investors are rarely able to focus on the long term, especially during periods of uncertainty in the equity markets, regardless of their actual investment time horizon.

During shorter time frames there are often periods of economic weakness that impact markets and an investor is likely to react differently depending on their asset allocation – a balanced investor might experience less of a drop in the value of their portfolio, since bonds have historically provided a counterweight to weakness in equities.

According to industry data2, equity fund outflows typically increase during periods of market turmoil and usually occur after the initial market pullback. So much for “buy low, sell high”. Emotionally, a balanced investor is likely to feel less anxious and inclined to sell relative to an investor with a pure equity portfolio that doesn’t have the protection of bonds.

On paper, it makes sense for investors with longer time horizons to hold more equities. But in reality, it doesn’t consider that investors tend to be irrational and likely to react in the short term by “selling low”. A balanced asset allocation usually provides investors with a smoother investment experience and perhaps helps protect them from selling equities after they have already fallen in price.

Bonds typically offer a measure of downside protection during periods of weakness in equities. By reducing the decline in the value of the portfolio, investors may have more capital to reallocate to equities at attractive valuations. If you believe that we are likely to enter a period of further economic weakness, we’re likely to be reminded of the importance of bonds in a portfolio.

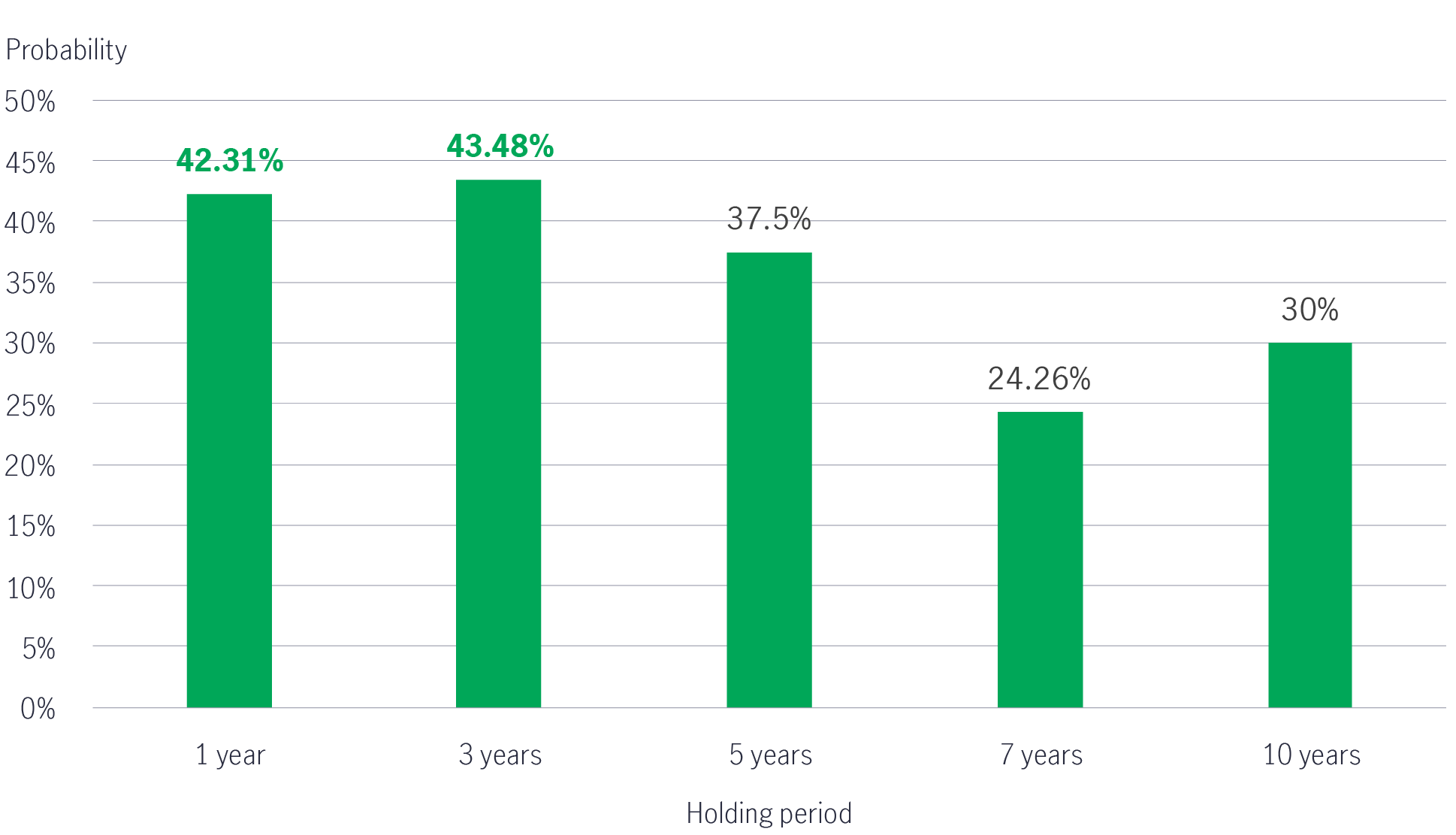

Regarding historical performance, the probability of Asian bonds outperforming Asia Pacific ex-Japan equities was around 42% and 43% when held for one year and three years, respectively3. Similar results were seen in global bonds, with the probability of this asset class outperforming global equities within 7-year and 15-year holding periods at over 43%4.

Historical data analysis: The probability of Asian bonds outperforming Asia Pacific ex Japan equities3

Historical data analysis: The probability of global bonds outperforming global equities4

While what we see on paper may be true, we also have to look at what happens in reality. Two things that seem contradictory (bonds can outperform/underperform equities in the long-term) can be true at once. Context matters.

1 Since 2007 to 2022 (16 years), MSCI World Index (Global Equities) outperformed Bloomberg Barclays Global Index (Global Bonds) in 11 calendar years.

2 Morningstar, 31 December 2023.

3 Manulife Investment Management and Bloomberg, as of 31 December 2023. Data periods: 30 September 2005 – 31 December 2023. Rolling monthly total returns in US dollars. Asian bonds are represented by a blend of 50% JPMorgan Asia Credit Index and 50% HSBC Asian Local Bond Index (2005 to 2012)/Markit iBoxx Asian Local Bond Index (2013 to 2023). Asia Pacific ex-Japan equities are represented by the MSCI Asia Pacific ex-Japan Index. Past performance is not indicative of future performance.

4 Manulife Investment Management and Bloomberg, as of 31 December 2023. Data periods: 31 January 1990 – 31 December 2023. Rolling monthly total returns in US dollars. Global bonds are represented by the Bloomberg Barclays Global Aggregate Index. Global equities are represented by the MSCI World Index. Past performance is not indicative of future performance.

What is Better Income?

By adopting the Better Income approach, investors can tailor their portfolios to meet their financial goals while managing risk effectively when income investing.

Risk Diversification

There is no free lunch. But Risk Diversification comes close in investing. A diversified portfolio was shown to optimize returns with lower volatility in the long run.

Better income – Aim for higher, not the highest

If we focus too much on chasing the highest yield and upfront yield generation, we could suffer from early capital depletion and miss the total return opportunity towards the later stages of the investment journey.

Cash is king?

Amid volatile market conditions and higher interest rates, seeking security by burying your savings in a deposit account is tempting. As the saying goes, “cash is king”. Or is it?

© 2025 Manulife Investment Management. All rights reserved.